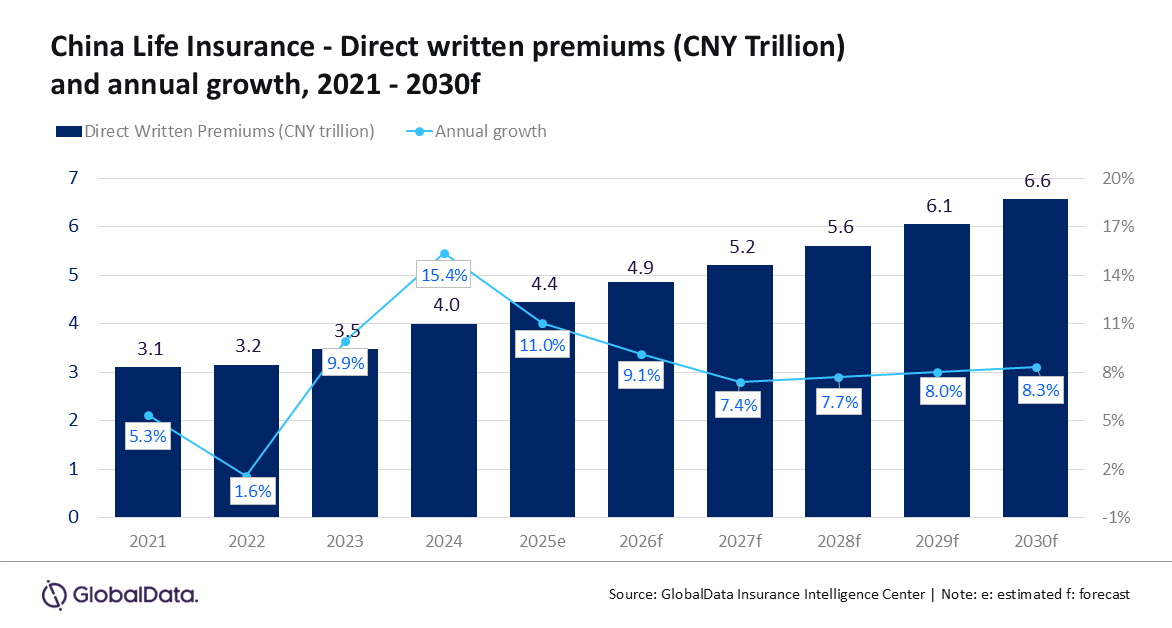

China life premiums projected to rise from $679.5b in 2026 to $927.5b in 2030

This represents a CAGR of 7.9% in direct written premiums.

China’s life insurance market is expected to expand steadily over the next five years, rising from $679.5b in 2026 to $927.5b in 2030, according to GlobalData.

This represents a CAGR of 7.9% in direct written premiums.

GlobalData estimates that life insurance premiums will grow 11% in 2025.

The increase is driven by distribution reforms, product changes following the benchmark rate cut, and continued digitalisation that has made sales and claims handling more efficient.

Bancassurance has also strengthened after regulators removed the cap on bank partnerships in May 2024, accounting for about 60% of new premiums in the first half of 2025.

Demand continues to rise as China’s population ages. The National Bureau of Statistics expects people aged 60 and above to make up 22% of the population in 2025, with those over 65 reaching around 15%.

This shift is supporting whole life insurance, which is set to account for 81% of life insurance premiums in 2025.

High-net-worth customers are also using life insurance more actively for estate and inheritance planning.

China’s 15th five-year plan (2026–2030) aims to expand long-term care insurance, increase rural pensions, and strengthen financial resilience.

These measures, along with the gradual increase in the retirement age from 60 to 63 starting in 2025, are expected to support demand for life insurance over the medium term.

Insurers are also moving toward participating and universal life products to adjust to the lower benchmark rate of 1.99% for ordinary life products introduced in August 2025.

Companies are revising their product portfolios and accelerating new launches to meet the new pricing guidance.

Digital capabilities continue to advance as insurers adopt AI to improve underwriting, risk controls, and customer engagement. Whilst bancassurance and online channels are expanding quickly, the agent force is showing signs of stabilisation under the new NFRA framework, which includes tiered licensing and revised commission rules.

Swarup Kumar Sahoo, Senior Insurance analyst, notes that whilst new business may fluctuate in the near term as the market adjusts to lower guaranteed interest rates, the long-term outlook for China’s life insurance sector remains positive.

Advertise

Advertise